What is the responsibility of A Taxpayer

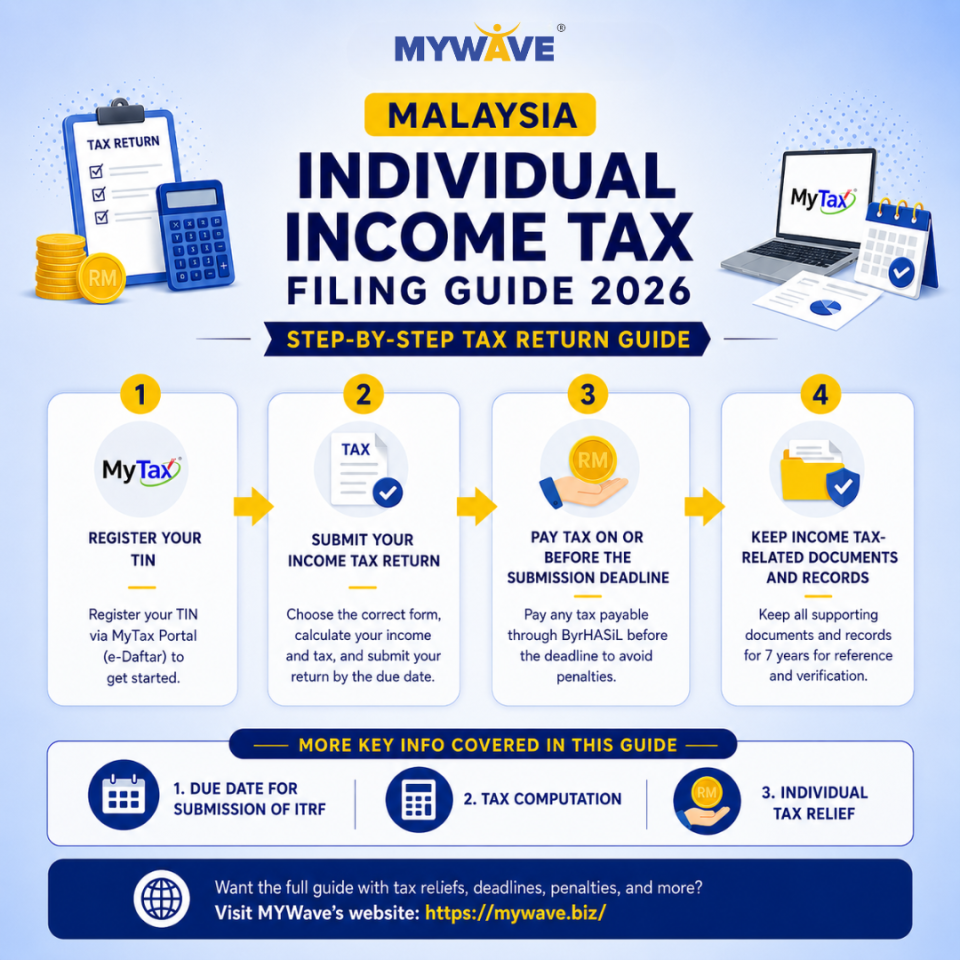

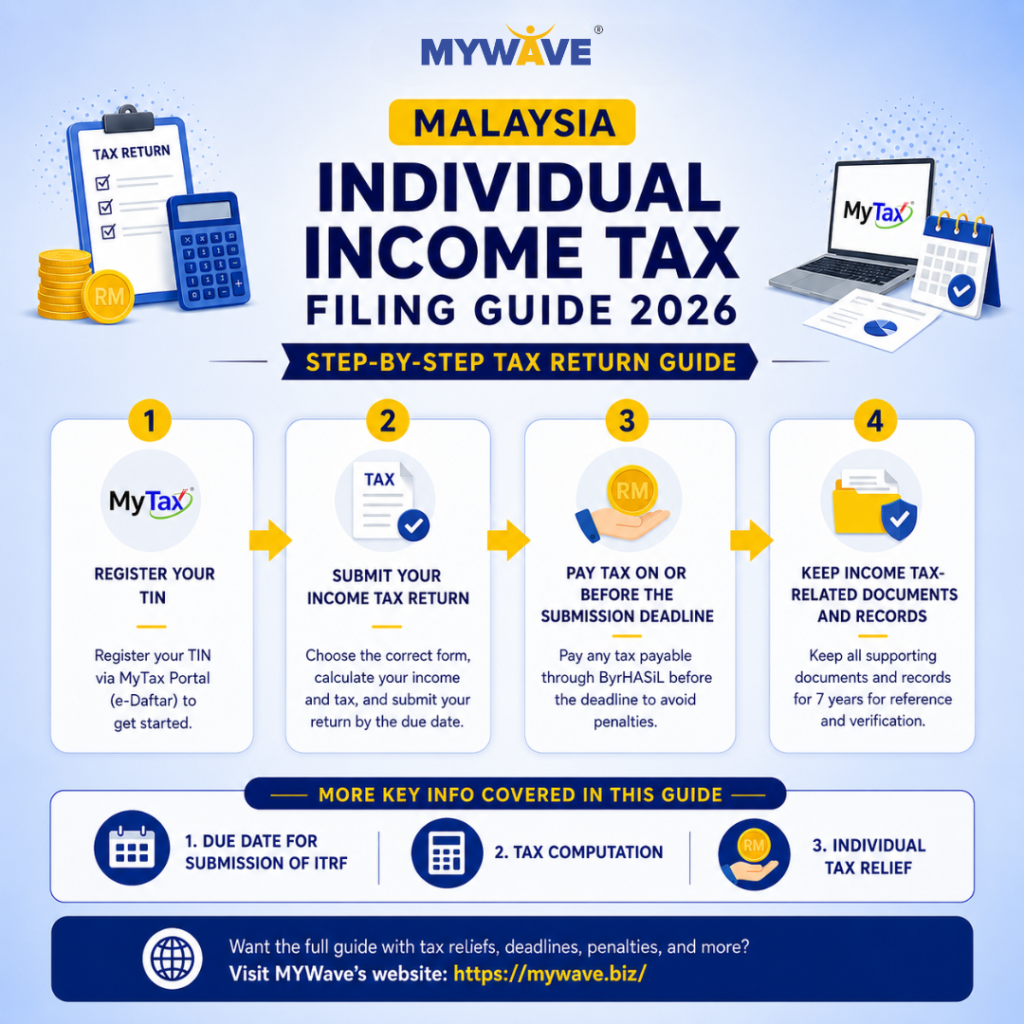

Step 1: Registration of Income Tax File Number & Update Personal Data

Step 2: Obtaining and forwarding Income Tax Return Form (ITRF)

Step 3: Tax Payment

Registration of Income Tax File Number

Q: “Do I need to register income tax file number?”

Yes, if you are fall under the below category:-

- An Individual, Single, who receiving yearly income RM34,001 (after deduct EPF)

- An Individual, Married with spouse not working, who receiving yearly income RM46,001

- An Individual who has business income

- An Individual who has sell / purchase of property

- An Individual who has PCB deduction

- An Individual who has earning need to pay for tax

Q: “How to register an income tax file number?”

- Submit online application to e-Daftar at http://edaftar.hasil.gov.my/index/index.php

- Submit CP600 application form to nearby Income Tax Office

- http://phl.hasil.gov.my/pdf/pdfborang/Borang_Daftar_Individu_1.pdf

- Type of document required:

- A copy of Identification card / police i.c. / army i.c. / international passport

- Company Registration Certificate (those with business income)

- CP600 form (for manual application only)

- Income Statement / Payslip (for manual application only)

Update Personal Data Changes

Q: “Do I need to notify LHDNM on changing of my particular?”

Yes, you may make the necessary update through the following method:-

- Online e-Kemaskini LHDNM: https://ez.hasil.gov.my/ci

- Feedback to Customer Care LHDNM : http://maklumbalas.hasil.gov.my/

- Submit CP600B Form (Change of Address Application Form) for updating your correspondence address. http://phl.hasil.gov.my/pdf/pdfborang/CP600B_Pin1_2018_1.pdf

Yearly Income Tax Declaration

Q: “After registration of tax file, what is the next step?”

- Obtaining and forwarding Income Tax Return Form (ITRF) by manual hardcopy form or online E-Filing

- Declaring wages and business source income inclusive of allowable deduction, relief and rebate

- Keeping all business records, supporting documents of deductions, reliefs and rebate for a period of 7 years.

- Example of supporting documents:

- Borang EA/li>

- Original dividend vouchers

- Insurance receipts

- Parent Medical bill

- Book/Laptop/Tablets

- Donation receipts

- Purchase Receipts

Q:”What type of Income Tax Return Form I need to submit?”

- Borang BE: Resident Individuals Who Do NOT Carry On Business

- Borang B: Resident Individuals Who Has Carry On Business

- Borang M: Non-Resident Individual

- Borang BT: Resident Individuals Who categorize as Knowledge / Expert Workers

- Borang MT:Non-Resident Individuals Who categorize as Knowledge / Expert Workers

Q: “When is the Due Date for Submission of Income Tax Return Form ?”

- Individuals who do not carry on business : before or on 30 April 2021

- Individuals who carry on business : before or on 30 June 2021

Q: “Any Grace Period?”

- e-Filing Borang BE: 15 days (15 May 2021)

- e-Filing Borang B: 15 days (15 May 2021)

Q: “I have only receive employment salary by early of the year and I have start my own small business mid of the year. Do I need to submit both Borang BE & Borang B?”

You only have to fill-in Borang B to declare both your wages and business source income. Due date of submission by 30 June 2021.

Q: “I have encountered mistake after submission of Income Tax Return Form, what should I do?”

(1) Amendment Submitted Before Deadline for Submission of Return Form

- The letter and supporting documents must be submitted to the branch that handles your tax file.

(2) Amendment Within 6 Months from Due Date for Submission of Form

- Only taxpayers who have submitted the ITRF on time are allowed to make self amendment, only once for each year of assessment.

- Submitting an Amended Return Form (ARF) within 6 months from the due date for submission of ITRF. (*ARF 2020 pending release by LHDNM)

- Self amendment on information or assessment to correct mistakes in the ITRF relating to :

- Income under declared / not declared

- Expenses / other claims over claimed

- Capital allowances / incentives / reliefs over claimed

- For amendments other than mentioned above, ARF is not required. He can forward a detailed letter on the mistakes made and enclose documents (purchase receipts, invoices, etc.) to the branch which handles his income tax file.

Tax Payment

Q: “How to pay outstanding tax after completed Income Tax Return Form?”

There are three type of Payment Method available:

(1) Online LHDNM ByrHasil: https://byrhasil.hasil.gov.my/

- Internet banking with the FPX associate

- VISA, Mastercard and American Express credit cards

(2) Appointed LHDNM Agents

- Over bank counter

- Internet banking

- Auto Teller Machine (ATM)

- Cash Deposit Machine (CAM)

- Cheque Deposit Machine

- Tele-Banking

(3) Direct make payment to LHDNM Counter

Q: “How to pay outstanding tax if I was at oversea?”

Payment of income tax through monetary transfer from overseas:

1. Telegraphic Transfer (TT) / Transfer Interbank Giro (IBG) / Electronic Fund Transfer (EFT)

Taxpayer have to call to get the payment procedure for tax payment via telegraphic transfer:

- HASIL Care Line: 03-8911 1000 (call within Malaysia) or 603-8911 1100 (call from oversea)

- Fax number: 603-6201 9637

- Email address: HelpTTpayment@hasil.gov.my

2. By Bank Draft

- Payable to : Director General of Inland Revenue

- Name and address of payer bank : Must be ‘local paying bank’ or ‘local correspondence bank’ so that the draft becomes a local cheque.

- Payer may purchase bank draft in other than Malaysian Ringgit (RM) currency.

- Payer has to ensure that the amount paid are accurate and exact based on the exchange rate on payment day.

- Payment will be recorded based on exchange rate on the day it was credited.

- Payment and payer details must be written clearly at the back page of the bank draft and posted to:

Inland Revenue Board Malaysia

Kuala Lumpur Payment Centre

Ground Floor, Block 8A

Government Offices Complex,

Jalan Tunku Abdul Halim

50600 KUALA LUMPUR, MALAYSIA

Q: “What is LHDNM payment code I should use for individual tax payment?”

| Payment Code> | Description |

|---|---|

| 084 | Tax Instalment Payment/Tax Balance – Individual |

| 095 | Income Tax Payment (excluding instalment scheme) |

Q: “When is the Due Date of Income Tax Payment?”

- Individuals who do not carry on business: before or on 30 April 2021

- Individuals who carry on business: before or on 30 June 2021

Q: “Can I request to Pay Tax Balance by Installment?”

- Forwarding a letter of appeal to the Collection Unit of the branch where your tax file is maintained.

- The said letter must be received by the Collection Unit before 30th April of the relevant year.

- Please note that even if the appeal is approved, late payment penalty will still be imposed.

Q: “What is the Penalty of Late Payment?”

- Penalty of 10% will be imposed on the balance of tax not paid after 30th April following the year of assessment.

- If the tax and penalty imposed is not paid within 60 days from the date the penalty is imposed, a further penalty of 5% will be imposed on the amount still owing.

Q: “How to Appeal On Late of Payment Penalty?”

- An appeal in writing to the relevant branch of the Collection Unit within 30 days from the date the Notice of Increased Assessment is issued.

- The penalty imposed has to be settled notwithstanding any appeal made. If the appeal is successful, IRBM will refund the relevant amount.

Q: “When can I receive my income tax return after tax filing?“

- 30 working days from the date of submission by E-Filing

- 90 working days from the date of submission by manual hardcopy form

Source from :

http://www.hasil.gov.my/bt_goindex.php?bt_kump=5&bt_skum=1&bt_posi=1&bt_unit=5000&bt_sequ=1

{kind=link}

{kind=link}

{kind=link}

{kind=link}