If you earn an income in Malaysia or employ staff, understanding how Malaysia’s income tax system works is more than just a legal obligation. It helps you avoid costly mistakes, ensure payroll compliance, and make informed financial decisions throughout the year.

Many employees only think about taxes when filing their annual return, while employers often assume payroll tax is simply about deducting Monthly Tax Deduction (MTD). In reality, Malaysia’s tax system involves much more, from determining taxable income to understanding employer obligations and maintaining accurate payroll records.

In this guide, we’ll explain how Malaysia’s income tax system works, who needs to pay income tax, what counts as employment income, and why proper payroll management is essential for tax compliance.

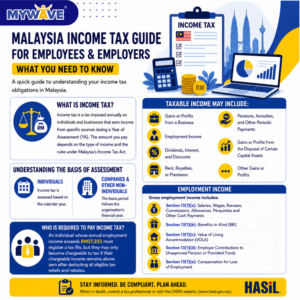

What Is Income Tax in Malaysia?

Income tax is a tax imposed annually on individuals and businesses that earn income from specific sources during a Year of Assessment (YA). The amount of tax you pay depends on the type of income you receive and the applicable tax rules under Malaysia’s Income Tax Act.

Taxable income in Malaysia may include the following:

- Gains or Profits from a Business

If you operate a sole proprietorship, partnership, or any business activity, the profits you earn are generally subject to income tax. Even if your business incurs a loss, you are still required to declare your business income in your annual tax return. - Employment Income

This refers to income earned through employment, including your basic salary, bonuses, commissions, allowances, overtime pay, director’s fees, and certain employee benefits provided by your employer. - Dividends, Interest, and Discounts

Income received from investments, such as dividends from shares, interest earned from certain financial products, or discounts that qualify as taxable income, may be subject to tax depending on the applicable tax treatment and exemptions. - Rent, Royalties, or Premiums

Rental income from properties, royalties received from intellectual property such as books, music, patents, or trademarks, as well as certain premium payments, are generally considered taxable income. - Pensions, Annuities, and Other Periodic Payments

Regular payments received after retirement or through long-term financial arrangements may be taxable, depending on the source of the income and any available exemptions under Malaysian tax laws. - Gains or Profits from the Disposal of Certain Capital Assets

Certain gains arising from the disposal of capital assets may be subject to tax under Malaysia’s Capital Gains Tax (CGT) rules, depending on the type of asset and the prevailing legislation. - Other Gains or Profits

The Income Tax Act also covers other forms of income that do not fall under the categories above but are specifically treated as taxable under Malaysian tax law.

Regardless of the source of income, every taxpayer is responsible for accurately declaring their taxable income, claiming eligible tax reliefs, and paying any tax due under Malaysia’s self-assessment system.

Understanding the Basis of Assessment

One area that often causes confusion is the basis of assessment, which differs for individuals and businesses.

Individuals

For individuals, income tax is assessed based on the calendar year.

For example:

- Year of Assessment (YA) 2024 covers income earned between 1 January 2024 and 31 December 2024.

This means all employment income received during that calendar year is assessed for YA 2024.

Companies and Other Non-Individuals

For companies, co-operatives and trust bodies, the basis period generally follows the organisation’s financial year.

For example:

- If a company’s financial year ends on 30 June 2024, that financial year becomes the basis period for YA 2024.

Understanding this distinction is important when preparing financial statements and corporate tax filings.

Malaysia’s Self-Assessment Tax System

Malaysia adopts a self-assessment system, meaning taxpayers are responsible for determining their own tax liability, reporting their income correctly, claiming eligible tax reliefs, and filing their annual income tax return.

Who Is Required to Pay Income Tax?

Not everyone who earns an income automatically pays income tax.

An individual whose annual employment income exceeds RM37,333 must register a tax file, but they may only become chargeable to tax if their chargeable income remains above zero after deducting all eligible tax reliefs and rebates. Monthly Tax Deduction (MTD) serves as a prepayment of income tax during the year, but the final tax payable is determined after submitting the annual income tax return.

For individuals operating a business, income must still be declared even if the business records a loss during the year.

Employment Income

If you perform your employment duties in Malaysia, you are generally taxed on the income earned from that employment. This applies even if part of your salary is paid from outside Malaysia or your employer does not have an office or business presence in Malaysia. In other words, the source of payment or the employer’s location does not necessarily determine whether your employment income is taxable. Instead, what matters is that the employment is exercised in Malaysia.

Gross employment income includes the following:

Section 13(1)(a): Salaries, Wages, Bonuses, Commissions, Allowances, Perquisites and Other Cash Payments

This covers all forms of remuneration received in return for your employment. Besides your monthly salary, it includes bonuses, overtime pay, commissions, director’s fees, allowances, incentives, gratuities, rewards, and any other payment made in cash or that can be converted into cash. Essentially, if it is a financial reward for your work, it is generally considered part of your employment income.

Section 13(1)(b): Benefits-in-Kind (BIK)

Benefits provided by an employer in the form of goods or services may also be taxable. Common examples include the private use of a company car, mobile phone, driver, domestic helper, or other assets provided for personal benefit. These benefits are assigned a taxable value based on guidelines issued by the Inland Revenue Board of Malaysia (LHDN).

Section 13(1)(c): Value of Living Accommodation (VOLA)

If your employer provides accommodation, such as a house, apartment, condominium, or other residential property, the value of that accommodation may form part of your taxable employment income. The taxable amount is determined according to valuation rules prescribed under the Income Tax Act and relevant LHDN guidelines.

Section 13(1)(d): Employer Contributions to Unapproved Pension or Provident Funds

Employer contributions made to pension, provident funds, schemes, or societies that have not been approved by the Director General of Inland Revenue are treated as part of the employee’s gross employment income and become taxable only when a refund or payment from the fund is received by the employee.

Section 13(1)(e): Compensation for Loss of Employment

Compensation received due to the termination of employment, redundancy, retrenchment, or other forms of job loss is included as employment income. However, certain exemptions may apply depending on the reason for the termination and the amount received, as provided under the Income Tax Act and current exemption orders.

Understanding what constitutes employment income is important because it directly affects your taxable income, Monthly Tax Deduction (MTD), and annual income tax filing. Both employees and employers should ensure that all taxable benefits and remuneration are reported accurately to remain compliant with Malaysian tax regulations.

Here’s What MYWave Thinks

One of the most common payroll issues we encounter is the misconception that tax compliance only matters during annual tax filing. In reality, compliance starts with every payroll run. Incorrect employee classifications, missed taxable benefits, inaccurate allowances, or manual payroll errors can accumulate throughout the year and become much more difficult to rectify later.

At MYWave, we help Malaysian businesses simplify payroll processing while ensuring statutory deductions, payroll calculations, and tax-related reporting are handled accurately. Whether through our cloud HR and payroll system or our payroll outsourcing services, businesses can reduce administrative burden and stay focused on growth with greater confidence.

Conclusion

Understanding Malaysia’s income tax system is essential for both employees and employers. Knowing what income is taxable, how the self-assessment system works, and how employment income is calculated can help avoid compliance issues and improve financial planning. For employers, accurate payroll management plays a vital role in ensuring tax compliance throughout the year. Investing in reliable payroll processes not only reduces errors but also helps businesses meet their statutory obligations efficiently.

If you’re looking to simplify payroll management while staying compliant with Malaysian tax regulations, MYWave provides comprehensive payroll outsourcing and cloud HR payroll solutions designed to support businesses of all sizes. Contact our team to learn more.

👉 Simplify payroll management while staying compliant with Malaysian tax regulations.

Contact us now. https://mywave.biz/contact-us/

{kind=link}

{kind=link}

{kind=link}

{kind=link}