Filing your individual income tax is an important responsibility for every taxpayer in Malaysia. Understanding what is required, knowing which tax return form to submit, and meeting the submission deadlines can help ensure a smooth tax filing process.

This guide provides a straightforward overview of taxpayer responsibilities, explains which tax return forms to use, and walks through the basic tax filing process—from registering a Tax Identification Number (TIN) to calculating taxable income and tax payable.

Responsibility of a Taxpayer

Every taxpayer has several important responsibilities throughout the income tax filing process. These responsibilities help ensure that income is properly declared and supporting records are available whenever required.

1. Register for a Tax Identification Number (TIN)

Before submitting an income tax return, a taxpayer must first register for a Tax Identification Number (TIN).

The TIN serves as the taxpayer’s unique identification number for income tax administration purposes.

2. Declare Income by Submitting the Return Form (RF)

Taxpayers are responsible for declaring their income by submitting the appropriate Return Form (RF).

Depending on the taxpayer’s circumstances, this may include:

- Form BE

- Form M

The appropriate form should be completed and submitted according to the applicable requirements.

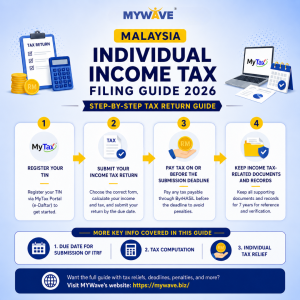

3. Pay Tax on or Before the Submission Deadline

After submitting the tax return, any tax payable should be settled on or before the deadline for submitting the Return Form.

Paying within the stipulated period helps avoid additional charges arising from late payment.

4. Keep Income Tax Documents and Records for Seven (7) Years

Taxpayers are required to keep income tax-related documents and records for seven (7) years to support the information declared in the Return Form.

These records may be required as proof of the information submitted during tax filing.

Submission of Tax Return Form

Submitting the correct Income Tax Return Form (ITRF) is an important part of the tax filing process.

The following forms apply to individual taxpayers:

| Form | Applicable To |

| Form BE | Resident individual who does not carry on business |

| Form M | Non-resident individual |

Explanatory notes and the relevant forms can be downloaded from the official HASiL website:

https://www.hasil.gov.my/en/muat-turun-borang/muat-turun-borang-individu/

Simple Guide on Tax Filing

The tax filing process can generally be divided into four main steps.

Step 1: Register Your Tax Identification Number (TIN)

Registration can be completed through the e-Daftar service available in the MyTax Portal.

Registration Process

1. Visit the MyTax Portal

2. Click Perkhidmatan ezHasil, then select e-Daftar

The system will redirect you to the Registration of T.I.N page.

3. Complete the Registration

On the registration page:

- Select the taxpayer type.

- Enter a valid identification number.

- Click Search.

If the reference number entered is valid and has not been registered, the system will display the e-Daftar link. You may proceed by clicking the link to complete the registration.

If the identification number has already been registered with LHDNM, taxpayers may proceed with the registration of the digital certificate through:

- e-CP55D, or

- e-KYC

Step 2: Submit Your Income Tax Return

Once a Tax Identification Number has been obtained, taxpayers may proceed to submit the appropriate Income Tax Return Form (ITRF).

This includes understanding the applicable submission deadline as well as completing the tax computation before submission.

Due Date for Submission of Income Tax Return Form (ITRF)

Different return forms have different submission deadlines depending on whether the taxpayer carries on a business.

| Forms |

Does Not Carry On Business |

Carry On Business |

| e-BE – Individuals with non-business income |

30 April |

— |

| e-B – Individuals with business income |

— |

30 June |

| e-P – Partnership (if related) |

— |

30 June |

| e-BT – Knowledge worker |

30 April |

30 June |

| e-M – Non-resident |

30 April |

30 June |

| e-MT – Non-resident (knowledge worker) |

30 April |

30 June |

| e-TP – Deceased person’s estate |

30 April |

30 June |

| e-C – Company |

30 April |

30 June |

| e-C1 – Cooperative |

30 April |

30 June |

| e-TF – Association |

30 April |

30 June |

The applicable deadline depends on the type of Income Tax Return Form being submitted. Taxpayers should ensure that their return is submitted within the prescribed timeframe.

Tax Computation

Before submitting the Income Tax Return Form, taxpayers need to compute both their taxable income and the amount of tax payable.

The tax computation generally involves two stages:

- Calculating taxable income

- Calculating tax payable

Calculating Taxable Income

Taxable income is determined by aggregating the relevant sources of income before deducting eligible donations, gifts, and tax reliefs.

| RM | RM | |

| Employment | XX | |

| Dividends | XX | |

| Interest, Discounts | XX | |

| Rents, Premiums, Royalties | XX | |

| Pensions, Annuities, Other Periodical Payment | XX | |

| Aggregate Income | XXX | |

| Less: Donations / Gift | (XX) | |

| Total Income | XXX | |

| Less: Tax Reliefs | (XX) | |

| Taxable Income | XXX |

This simplified illustration shows the sequence used in determining taxable income before tax is calculated.

Calculating Tax Payable

After determining taxable income, the next step is calculating the amount of tax payable.

| RM | RM | |

| Taxable Income | XXX | |

| Tax Charged (as per tax rate schedule) | XX | |

| Less: Tax Rebate | (X) | |

| Tax Payable | XX | |

| Less: MTD | (XX) | |

| Installment | (X) | |

| Balance of Tax Payable | XX |

The tax payable is determined after applying the applicable tax charged, tax rebate (where applicable), and deducting any Monthly Tax Deduction (MTD) or instalment payments that have already been made.

Tax Relief

Tax relief helps reduce your taxable income by allowing eligible deductions based on expenses or contributions that meet the qualifying conditions set by the Inland Revenue Board of Malaysia (HASiL). Taxpayers should ensure that every claim is supported by the required records and complies with the eligibility requirements.

The following categories are based on the official HASiL Tax Reliefs for the Year of Assessment 2025.

Individual

| Tax Relief |

Maximum Relief (RM) |

| Individual and dependent relatives |

9,000 |

| Disabled individual |

7,000 |

|

Education fees

|

7,000 |

| Husband/Wife/Payment of alimony |

4,000 |

| Disabled husband/wife |

6,000 |

|

Interest on Housing Loan – First Home Ownership (Sales and Purchase Agreement from 1st January 2025 to 31st December 2027) Relief Limit

|

RM7,000 |

Medical & Special Needs

| Tax Relief |

Maximum Relief (RM) |

|

Medical expenses for self, spouse or child

|

10,000 |

|

Expenses for parents and grandparents

|

8,000 |

| Expenditure on basic support equipment for disabled individual (Self/spouse/child/parent) |

6,000 |

Lifestyle

| Tax Relief |

Maximum Relief (RM) |

|

Lifestyle expenses (Self/spouse/child)

|

2,500 |

|

Additional lifestyle relief

|

1,000 |

| Electric vehicle charging equipment and domestic food waste composting machine (For household use) |

2,500 |

Insurance & Contributions

| Tax Relief |

Maximum Relief (RM) |

| Life insurance, EPF and qualifying contributions |

7,000 |

| Deferred Annuity and Private Retirement Scheme (PRS) |

3,000 |

| Education and medical insurance (Self/spouse/child) |

4,000 |

| Net deposit into SSPN (Claimable by husband/wife) |

8,000 |

| SOCSO contributions |

350 |

Child Relief

| Tax Relief |

Maximum Relief (RM) |

| Child below 18 years of age – unmarried |

2,000 |

|

Child aged 18 years of age

|

8,000 |

|

Child aged 18 years of age

|

2,000 |

| Unmarried child with disabilities |

8,000 |

|

Additional relief

|

8,000 |

|

Registered childcare centre (TASKA)/Kindergarten (TADIKA) fees

|

3,000 |

|

Purchase of breastfeeding equipment

|

1,000 |

For the latest qualifying conditions and detailed eligibility requirements for each relief, taxpayers should refer to the official HASiL Tax Relief guidance.

Late or Failure to Submit the Return Form

Submitting the Income Tax Return Form within the prescribed deadline is an important taxpayer responsibility.

Where the Return Form is submitted after the due date or after an approved extension period, a penalty may be imposed based on:

- The length of time after the due date or approved extension.

- The amount of tax imposed.

The applicable penalty rates are:

| Period After Due Date |

Penalty |

| Up to 12 months |

15% |

| Exceeding 12 months up to 24 months |

30% |

| Exceeding 24 months |

45% |

Submitting the Return Form on time helps taxpayers avoid these additional penalties.

Step 3: Pay Tax on or Before the Submission Deadline

After submitting the Income Tax Return Form, taxpayers are required to pay any tax payable on or before the submission deadline.

Tax payments can be made through the ByrHASiL Service:

https://byrhasil.hasil.gov.my/HITS_EP/

Making payment within the prescribed period helps ensure compliance with income tax obligations.

Late or Failure to Pay Tax

Where tax remains unpaid after the prescribed due date or approved extension period, an increment will be imposed.

|

Situation |

Increment |

|

Late payment of tax payable |

10% of the tax payable |

Paying any outstanding tax before the deadline helps avoid this additional charge.

Step 4: Keep Income Tax-Related Documents and Records

Taxpayers are required to keep income tax-related documents and records for seven (7) years as supporting evidence for the information declared in their Income Tax Return Form.

Examples of records include:

- EA Form

- List of entries and exit

- Copy of passport together with the original for verification (if required)

- Copy of departure flight ticket (if required)

- Other related documents such as invoices, receipts, EPF statements, zakat records and other supporting documents

Maintaining complete records helps support the information declared should verification be required.

MYWave Can Help Simplify Payroll and Tax Compliance

Accurate payroll records play an important role in supporting employees during tax filing. Documents such as EA Forms, payroll records, statutory contribution records, and other employment-related information are essential when preparing an Income Tax Return.

MYWave helps Malaysian businesses streamline payroll administration through its comprehensive HR and payroll solutions, enabling employers to maintain accurate payroll records, generate statutory reports, and support compliance with Malaysian payroll requirements. By ensuring payroll information is properly managed throughout the year, businesses can better support employees during the annual income tax filing process.

Conclusion

Understanding your responsibilities as a taxpayer is the first step towards meeting your income tax obligations. From registering a Tax Identification Number (TIN) and submitting the correct Income Tax Return Form to calculating taxable income, claiming eligible tax reliefs, paying tax on time, and maintaining proper records, each step contributes to a smoother tax filing process.

For businesses, maintaining accurate payroll records throughout the year makes tax reporting significantly more efficient. MYWave’s HR and payroll solutions help organisations manage payroll accurately, generate essential employment records, and support ongoing statutory compliance, allowing employers and employees to approach tax filing with greater confidence.

If your organisation is looking for a trusted HR and payroll partner in Malaysia, MYWave provides a complete HR, payroll, and workforce management ecosystem designed to simplify payroll administration and support statutory compliance throughout the year.

👉 Contact Us Now!

Reach out to us at: https://mywave.biz/contact-us/

{kind=link}

{kind=link}

{kind=link}

{kind=link}